Cosmetics company e.l.f. Beauty (NYSE:ELF) met Wall Street’s revenue expectations in Q2 CY2025, with sales up 9% year on year to $353.7 million. On the other hand, next quarter’s revenue guidance of $328.2 million was less impressive, coming in 8.5% below analysts’ estimates. Its non-GAAP profit of $0.89 per share was 6.4% above analysts’ consensus estimates.

Is now the time to buy e.l.f. Beauty? Find out by accessing our full research report, it’s free.

e.l.f. Beauty (ELF) Q2 CY2025 Highlights:

- Revenue: $353.7 million vs analyst estimates of $353.7 million (9% year-on-year growth, in line)

- Adjusted EPS: $0.89 vs analyst estimates of $0.84 (6.4% beat)

- Due to the "wide range of potential outcomes related to tariffs, the Company is not providing a full year Fiscal 2026 financial outlook at this time"

- Operating Margin: 13.8%, down from 15.6% in the same quarter last year

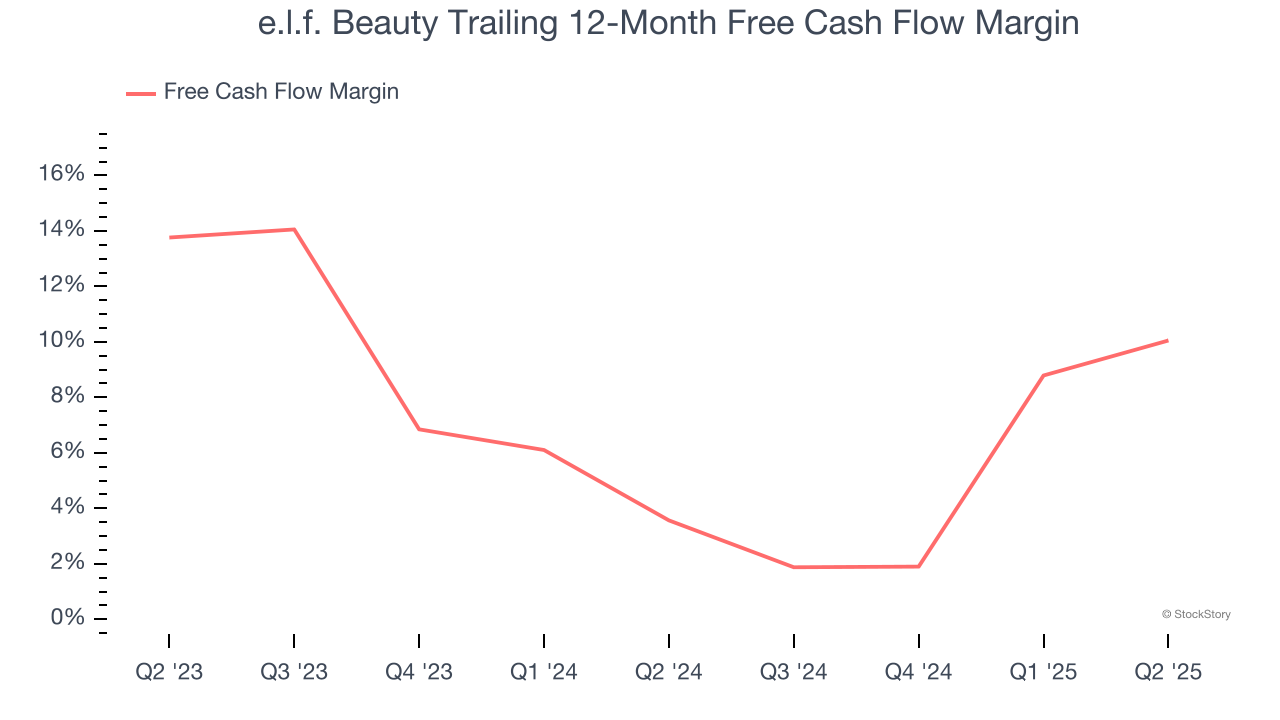

- Free Cash Flow Margin: 5.7%, up from 0.2% in the same quarter last year

- Market Capitalization: $6.23 billion

“Our strong Q1 results, including 210 basis points of market share gains, are a continuation of the consistent, category-leading growth we’ve delivered over the past 26 quarters,” said Tarang Amin, e.l.f.

Company Overview

Short for "eyes, lips, face", e.l.f. Beauty (NYSE:ELF) is a developer of high-quality beauty products at accessible price points.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.34 billion in revenue over the past 12 months, e.l.f. Beauty is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, e.l.f. Beauty’s sales grew at an incredible 47.6% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows e.l.f. Beauty’s demand was higher than many consumer staples companies.

This quarter, e.l.f. Beauty grew its revenue by 9% year on year, and its $353.7 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 26.6% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is healthy and implies the market is forecasting success for its products.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

e.l.f. Beauty has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.1% over the last two years, better than the broader consumer staples sector.

Taking a step back, we can see that e.l.f. Beauty’s margin expanded by 6.5 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

e.l.f. Beauty’s free cash flow clocked in at $20.14 million in Q2, equivalent to a 5.7% margin. This result was good as its margin was 5.5 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from e.l.f. Beauty’s Q2 Results

Revenue was just in line and operating margin also declined noticeably year on year. Due to the "wide range of potential outcomes related to tariffs, the Company is not providing a full year Fiscal 2026 financial outlook at this time". This added uncertainty to the near-term outlook, something the market dislikes, and as a result, the stock traded down 11.8% to $97.40 immediately following the results.

Is e.l.f. Beauty an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.